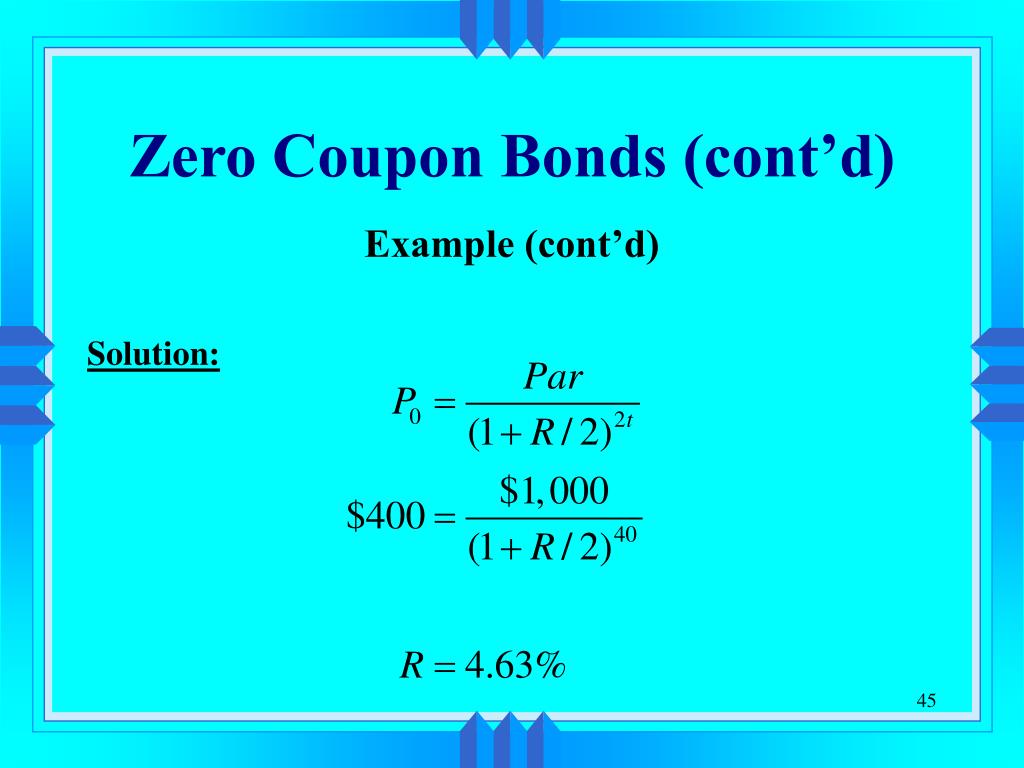

40 define zero coupon bond

What Is Bond Yield? - Investopedia May 31, 2022 · Bond Yield: A bond yield is the amount of return an investor realizes on a bond. Several types of bond yields exist, including nominal yield which is the interest paid divided by the face value of ... Bootstrapping Zero Curve & Forward Rates ... Oct 22, 2016 · The discounted cash flows & zero rates for later tenors will be solved for using the par bond assumption and the zero rates derived for the earlier tenors. This is illustrated in the steps that follow. 5. Let us start with the shortest tenor bond, the 0.25 year bond. Its cash flows are coupon and principal payable at maturity of 101.0075.

Answered: Define each of the following terms:c.… | bartleby A: A zero-coupon bond is also known as accrual bond because a zero coupon bond doesn't pay the coupon… Q: The discount bond sells for ____________ as maturity approaches. A: Bond is a debt instrument issued by companies and government.

Define zero coupon bond

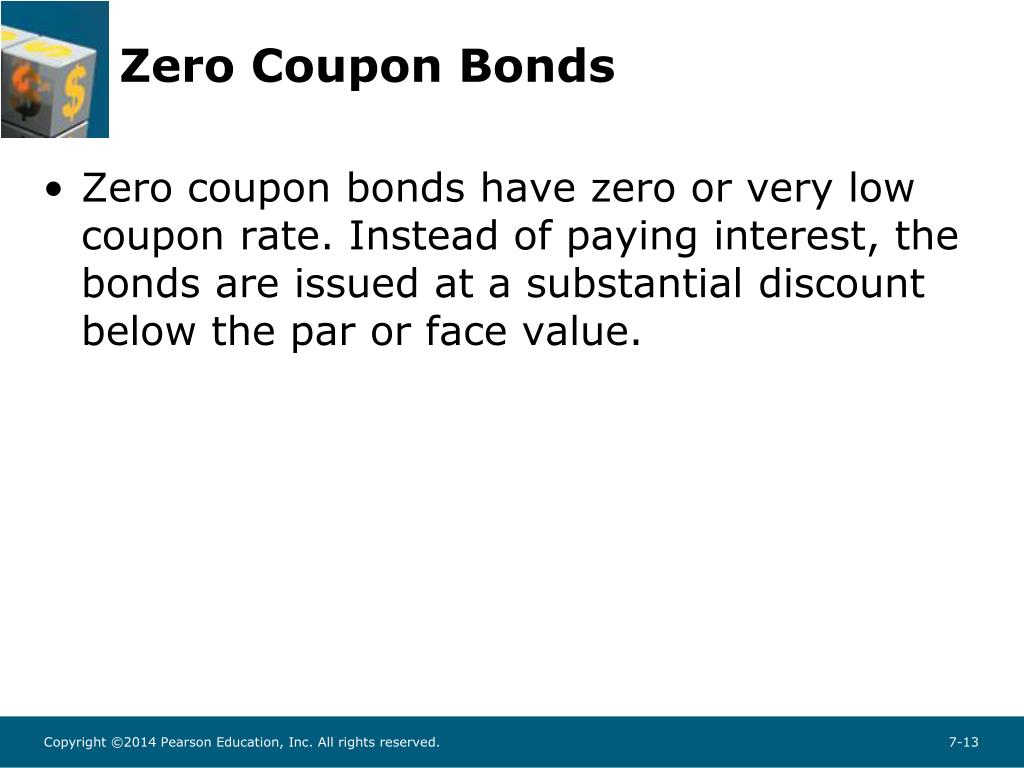

Zero Coupon Bond | Investor.gov Zero Coupon Bond Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due. The maturity dates on zero coupon bonds are usually long-term—many don’t mature for ten, fifteen, or more years. Bond Definition: What Are Bonds? – Forbes Advisor Aug 24, 2021 · Coupon: The fixed rate of interest that the bond issuer pays its bondholders. Using the $1,000 example, if a bond has a 3% coupon, the bond issuer promises to pay investors $30 per year until the ... Warrant (finance) - Wikipedia Warrants are issued in this way as a "sweetener" to make the bond issue more attractive and to reduce the interest rate that must be offered in order to sell the bond issue. Example. Price paid for bond with warrants ; Coupon payments C; Maturity T; Required rate of return r; Face value of bond F

Define zero coupon bond. Convexity of a Bond | Formula | Duration | Calculation The number of coupon flows (cash flows) change the duration and hence the convexity of the bond. The duration of a zero bond is equal to its time to maturity, but as there still exists a convex relationship between its price and yield, zero-coupon bonds have the highest convexity and its prices most sensitive to changes in yield. Warrant (finance) - Wikipedia Warrants are issued in this way as a "sweetener" to make the bond issue more attractive and to reduce the interest rate that must be offered in order to sell the bond issue. Example. Price paid for bond with warrants ; Coupon payments C; Maturity T; Required rate of return r; Face value of bond F Bond Definition: What Are Bonds? – Forbes Advisor Aug 24, 2021 · Coupon: The fixed rate of interest that the bond issuer pays its bondholders. Using the $1,000 example, if a bond has a 3% coupon, the bond issuer promises to pay investors $30 per year until the ... Zero Coupon Bond | Investor.gov Zero Coupon Bond Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due. The maturity dates on zero coupon bonds are usually long-term—many don’t mature for ten, fifteen, or more years.

#zerocouponbonds #Bonds Zero Coupon Bonds - Meaning, Formula, Pros ...

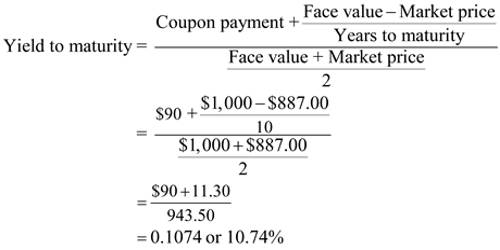

Yield To Maturity Formula / Professional Bond Valuation and Yield to ...

How to Calculate the Yield of a Zero Coupon Bond Using Forward Rates?

Understanding Zero Coupon Bonds

PPT - Measurement of Interest Rate Risk PowerPoint Presentation, free ...

ZERO COUPON BOND CALCULATOR - BOND CALCULATOR - AIR MILE CALCULATOR

Part+3+Financial+securities+-+Chapter+6++7(1) - Part 3 Financial ...

PPT - Chapter 2 Bond Prices and Yields PowerPoint Presentation - ID:2716955

Understanding Zero Coupon Bonds

Bond Prices and Yields CHAPTER 9 Bond Prices

Zero Coupon Bond - YouTube

united states - Can zero-coupon bonds go down in price? - Personal ...

Define zero coupon bond.(urdu/hindi) - YouTube

The term structure of interest rates

PPT - Chapter 12 Bond Prices and the Importance of Duration PowerPoint ...

Zero Coupon Bonds - YouTube

Bond Prices and Yields CHAPTER 9 Bond Prices

PPT - Chapter 7 The Valuation and Characteristics of Bonds PowerPoint ...

Post a Comment for "40 define zero coupon bond"